At Christianson, our objective is to make tax work as transparent as possible and easier for our clients to understand. This new Tax Reform Bill is the largest since the 1980s so there is a lot to take away from it. Our experts have provided an analysis of these changes (for both individuals and businesses) to help make the new tax laws easier to understand. If you have questions relating to this information, contact us and we will walk you through it!

What Changes Impact Individuals?

| Current Law | New Law | |

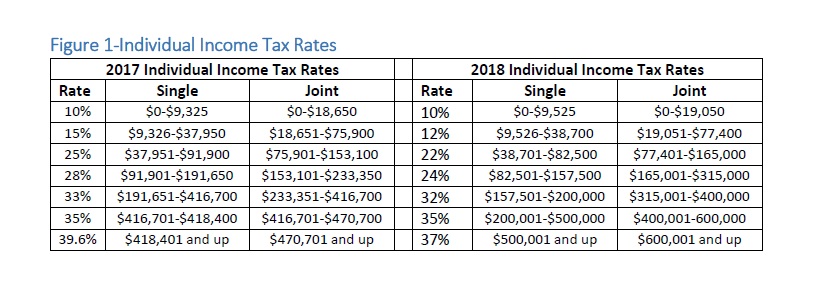

| Individual tax rates

See Figure 1 for details |

Seven tax brackets: 10%, 15%,

25%, 28%, 33%, 35%, 39.6% |

Seven tax brackets: 10%, 12%,

22%, 24%, 32%, 35%, 37% |

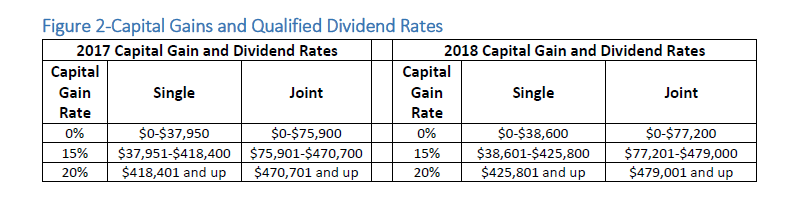

| Long-term capital gains and qualified dividend tax rates

See Figure 2 for details |

0%, 15%, 20% | Unchanged |

| Personal standard deduction | Married filing jointly: $12,700 Head of Household: $9,350

Single: $6,350 |

Married filing jointly: $24,000 Head of Household: $18,000

Single: $12,000 |

| Personal exemption | $4,050 | Repealed—no exemption |

| Child tax credit | $1,000 per child

Phase-out at MAGI of $110,000 MFJ, $75,000 single |

$2,000 per child (up to $1,400 refundable per child);

$500 for non-child dependents Phase-out increased to MAGI of $400,000 MFJ, $200,000 single |

| Personal state income, property tax and sales tax | Allowed as an itemized deduction | Combined deduction for property tax and either income

or sales tax limited to $10,000 |

| Mortgage interest | Deductible on up to $1.1 million of debt; interest on second home deductible | Deductible on up to $750,000 of debt (including second home); not home equity interest

deduction |

| Medical expenses | Deductible to the extent they exceed 10% of AGI | Deductible to the extent they exceed 10% of AGI (7.5% for

2017 and 2018) |

| Miscellaneous itemized deductions | Deductible for portion in excess of 2% of AGI floor | Deduction suspended for employee business expenses, uniforms, tax prep fees, professional dues, hobby loss, employee home office, tools

and supplies |

| Personal casualty loss | Itemized deduction allowed for personal casualty losses | Deduction for personal casualty loss eliminated (except federally declared disasters), theft loss

remains |

| Limit on itemized deductions | Overall limitation based on AGI | Repeals overall limitation |

| Moving expenses | Deduction allowed, qualified moving expense reimbursements excluded from

income. |

Both moving expenses and ability to exclude reimbursements from income

are repealed. |

| Individual Alternative Minimum Tax (AMT)

See Figure 3 for details |

Imposed when minimum tax exceeds regular income tax | Increases AMT exemption amounts and phase-outs |

| Alimony | Deductible to payor and taxable to recipient | Not deductible to payor, not taxable to recipient for decrees

executed or modified after 2018 |

| Individual health insurance mandate | Individuals subject to penalty for failure to have minimum essential health insurance

coverage |

Penalty repealed starting in 2019 |

| Exclusion of gain on sale of principal residence | Exclusion up to $250,000 ($500,000) for MFJ if 2 out of

previous 5 year test met |

No change |

| Excess business loss

See Figure 4 for details |

No provision | Net business losses over

$500,000 MFJ ($250,000 single) are not deductible; convert to NOL and carried over |

| Student loan discharged on

death or disability |

Included in gross income | Excluded from gross income |

| ABLE/529 accounts | No change on existing provisions | New provisions:

-Allows distributions up to $10,000 annually for elementary and high school tuition costs -Allows amounts from qualified tuition programs (529 plan) to be rolled to an ABLE account without penalty -Increased contribution to ABLE accounts |

| Repeal of IRA recharacterization rules | May recharacterize a contribution made during a year to a traditional IRA as a contribution to a Roth IRA, and vice versa, any time before the extended due date of the return for that year.

If a traditional IRA is converted to a Roth IRA during a year, the taxpayer can undo the conversion. |

IRA recharacterization rules will be repealed. Taxpayer may not unwind a Roth conversion. The repeal does not affect the rules for converting a traditional IRA to a Roth IRA. |

| Estate and gift | $5,490,000 gift or estate exemption per individual and

$5,490,000 GST exemption. |

Lifetime gift and estate tax exemption and the GST tax exemption will be doubled to

$11.2 million in 2018. The estate and GST taxes will not be repealed.

Planning will be focused on retaining the basis step-up. |

What Changes Impact My Business?

| Current Law | New Law | |

| Maximum pass-through tax rate

See Figure 5 for details |

39.6% | A deduction from ordinary rates of 20% of qualifying domestic

income; subject to limitations |

| Domestic Production Activities Deduction (DPAD)

See Figure 5 for discussion |

9% deduction of qualifying income for domestic producers | Repealed for tax years beginning after 12.31.17 |

| Maximum corporate tax rate | 35% | 21% |

| Corporate AMT | 20% | Repealed after 2017 with AMT

credits refundable |

| Net Operating Losses (NOL) | In general, 2 year carryback, 20 year carryforward | Carryback repealed, except 2 years for farms, with indefinite carryover deduction limited to

80% of income before NOL |

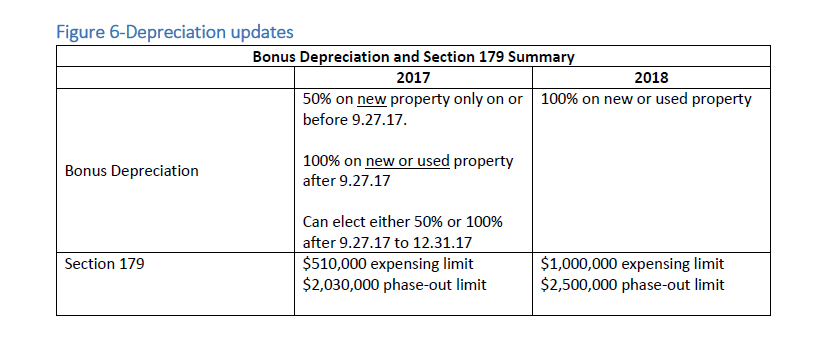

| Bonus Depreciation

See Figure 6 for details |

Deduct 50% of cost of new asset placed in service | Deduct 100% of new or used asset placed in service after

9.27.17 |

| Section 179

See Figure 6 for details |

Expense up to $510,000 of

assets placed in service Threshold of $2,030,000 |

Expense up to $1,000,000 with threshold of $2,500,000 |

| Farming asset lives | Seven years | Five years, with exceptions |

| Building depreciation | 27.5 years for residential rentals 39 years for most non-

residential buildings |

No changes |

| Real property improvements | Multiple criteria to meet to qualify for 15 year life | Changed to allow 15 year depreciation for all qualified

improvement property |

| Fringe benefits limited | Entertainment and recreation expenses not deductible unless a direct relationship to active

conduct of business |

No deduction will be allowed for entertainment, amusement, or recreational activity expenses |

| Business interest deduction | Deductible | Deduction limited to the extent interest exceeds 30% of income, with excess carried over. Not applicable if average annual gross receipts are less than

$25M. |

| Like-kind exchange treatment | Deferral of gain on both real and tangible personal property | Deferral on real property only. Like-kind exchange of tangible personal property will be taxable. Tax consequences should be limited as gain recognition on the disposition

of tangible personal property in an exchange adds to the basis of the replacement property which can be expensed under either Section 179 or 100% bonus depreciation. |

| Cash method of accounting | Limited to businesses with less than $1M, $5M or $10M in receipts, depending on other

factors |

Now includes businesses with less than $25M in receipts, with special inventory rules |

| Accounting for long-term contracts | Average annual gross receipts for prior 3 tax years not over

$10 million |

Expands exception for small construction contracts from the requirement to use the percentage of completion method by raising the $10 million gross receipts test limit to a $25 million gross receipts

test limit. |

| Taxable year of revenue recognition | Usually included in income no later than its actual or constructive receipt, unless properly accounted for in different period under the taxpayer’s accounting method. | Allows accrual method taxpayer to elect to defer the inclusion of income associated with certain advance payments to the end of the tax year following the year of receipt if it is also deferred for financial statement

purposes. |

| Deduction of research expenses | Deducted in year incurred | Will require capitalization and amortization over 5 years, effective for amounts paid or incurred in tax years beginning

after 2021. |

| New credit for employer-paid FMLA | No credit | For wages paid in 2018 and 2019, employer can claim a tax credit of 12.5% of wages paid to employees on FMLA if the rate of pay is 50% of wages normally paid. Credit increases for

payment over 50% |

| Technical terminations | Partnership terminates if sale or exchange of 50% or more of interests during 12 month

period |

Repealed |

We understand that this Tax Reform Bill is a bit complicated and not all of it will make sense to everyone, but please don’t hesitate to reach out to us with any questions you may have.

[button_1 text=”Contact%20Christianson%20Today!” text_size=”15″ text_color=”#ffffff” text_font=”Lato;google” text_letter_spacing=”1″ subtext_panel=”N” text_shadow_panel=”N” styling_width=”30″ styling_height=”20″ styling_border_color=”#ffffff” styling_border_size=”5″ styling_border_radius=”23″ styling_border_opacity=”100″ styling_gradient_start_color=”#1b335d” styling_gradient_end_color=”#1b335d” drop_shadow_panel=”N” inset_shadow_panel=”N” align=”center” href=”https://www.christiansoncpa.com/contact-us/”/]Disclaimer—This analysis is based on information available as of January 19, 2018 and is subject to

change as regulations and technical guidance are released. Though one of the last re-vote items sent

from the Senate back to the House was the elimination of the formal name of the legislation—The Tax Cuts and Jobs Act, we have used this term to reference the bill in this outline.

{kind=link}

{kind=link}

{kind=link}

{kind=link}